dfwford

Well-Known Member

- Joined

- Jan 23, 2023

- Threads

- 6

- Messages

- 717

- Reaction score

- 650

- Location

- Dallas, TX

- Vehicle(s)

- 2024 Ford Mustang GT Premium

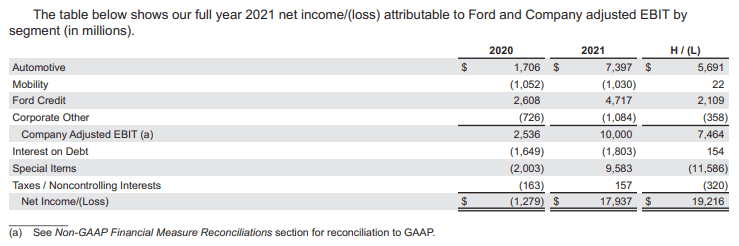

For a company that brings in $158 billion in revenue per year and has nearly 200K workers, a subsidiary with only $10 Billion in revenue and ~5,000 employees is definitely a tiny part of it.This is simply not true. Let's clear it up before people start believing it. I remember many years in the past where automakers earned more from financing than actually building and selling cars. For Ford, 2020 was such a year. Even in 2021, when Ford made more in the "Automotive" segment, there is no way you can call $4.7B a "relatively tiny portion of the company." It's not *that* hard to read an annual report.

https://s201.q4cdn.com/693218008/files/doc_financials/2021/ar/Ford-2021-Annual-Report.pdf

Granted, Ford Credit has been an extremely profitable operation for how small it is, and given the circus that is Ford's manufacturing/R&D operations right now (with all the failed launches / recalls and the supply chain pressures in part because of their abysmal relations with suppliers), you are correct that any little bit which helps to keep the broader company from as deep in the red as possible helps.

Sponsored

Last edited:

")