roadpilot

Well-Known Member

I literally just posted my CU's rates just above, and they are lower than 6.9%. ;)Lets put some money on this then….say $1,000.00 I can beat 6.9?

Sponsored

I literally just posted my CU's rates just above, and they are lower than 6.9%. ;)Lets put some money on this then….say $1,000.00 I can beat 6.9?

I promise not to use any of Sams money/incentives although both banks here that I use can (and are) beating 6.9. Pretty loyal to a CU in a northern statenot fair. Your Bank/CU of Sam Walton's Kids, has massive cash-flow to play with lending to it's local community.

Are you in for another $1,000.00I literally just posted my CU's rates just above, and they are lower than 6.9%. ;)

") .

.Term and amount also play a part. Sometimes that extra amount is lost when the customer elects to treat the provider the same.Are you in for another $1,000.00

I am sure there are some people out there with 800 credit score who do pay 6.9 or higher but if so they need to shop around more.

I agree with you 100% and those with a 800 scoreTerm and amount also play a part. Sometimes that extra amount is lost when the customer elects to treat the provider the same.

I agree with you 100% and even with a 800 score a 95% loan for 84 months will probably be over 6%.Term and amount also play a part. Sometimes that extra amount is lost when the customer elects to treat the provider the same.

Ah yeah the adm: assumed details matter clauseI agree with you 100% and those with a 800 score

I agree with you 100% and even with a 800 score a 95% loan for 84 months will probably be over 6%.

The “bet” was made that I would pay over 6.9% without knowing any of my loan terms and I have better rates than that already

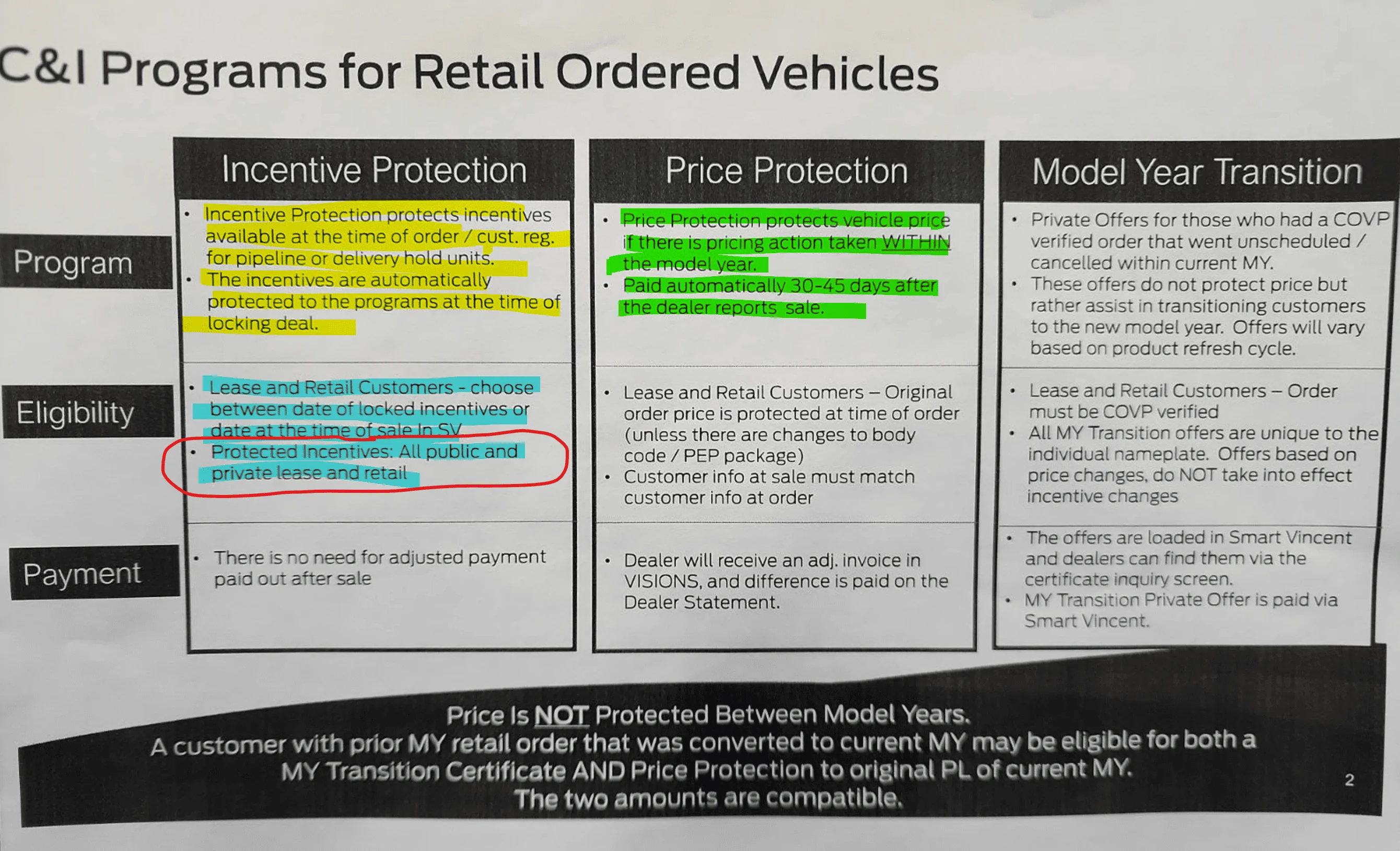

From my salesman. Applies to all incentives, including special financing, not just rebates. Also, price protection if the prices increase within the model year - worst case, you'll get a check after the deal rather than the price adjusted at the time of sale.That's just it, there is nothing in writing regarding price, rate, or term required to order a car. Therefor it's not locked.

You're actually most likely locked in for Program #20068. You have a choice of rates/terms, including the 1.9% for 36 months.Got my build notice of April 9th from my salesman last night so I went in the dealership to inquire about rates. Got locked in for 1.9% and even if rates go up before I take possession my rate will not go up. I am sure non of my other lenders can match this rate so Ford it is.

I tried getting locked in. My car will be delivered AFTER April 2nd. Sales rep said he couldn't do it.Got my build notice of April 9th from my salesman last night so I went in the dealership to inquire about rates. Got locked in for 1.9% and even if rates go up before I take possession my rate will not go up. I am sure non of my other lenders can match this rate so Ford it is.

Your sales rep either failed you (by not locking the program when you ordered it) or he's an idiot. Ford rebates AND Ford Credit financing available at the time of order ARE available unless you get pushed to the next model year.I tried getting locked in. My car will be delivered AFTER April 2nd. Sales rep said he couldn't do it.

I'll check with the sales manager. My sales rep is gonzo.Your sales rep either failed you (by not locking the program when you ordered it) or he's an idiot. Ford rebates AND Ford Credit financing available at the time of order ARE available unless you get pushed to the next model year.

Not sure when PGM #20068 started. You ordered back in DEC 2023, right?I'll check with the sales manager. My sales rep is gonzo.